Credit card payments have become a way of life for many Americans. Nearly 60% of families claim to use them for the convenience, and market innovations like Apple Pay have made it even easier to “charge it." While credit cards may be easy to use, they’re also easy to pile up debt with.

- Credit card debt grew near 6% year-over-year in Q2 2019 to $6,194 nationwide.

- Alaska, New Jersey and Connecticut lead the nation in credit card debt balances.

- Iowa, Wisconsin and Mississippi are the states with the lowest credit card burdens.

- The rise in credit card debt has led to double-digit revenue growth among many banks and credit card processors.

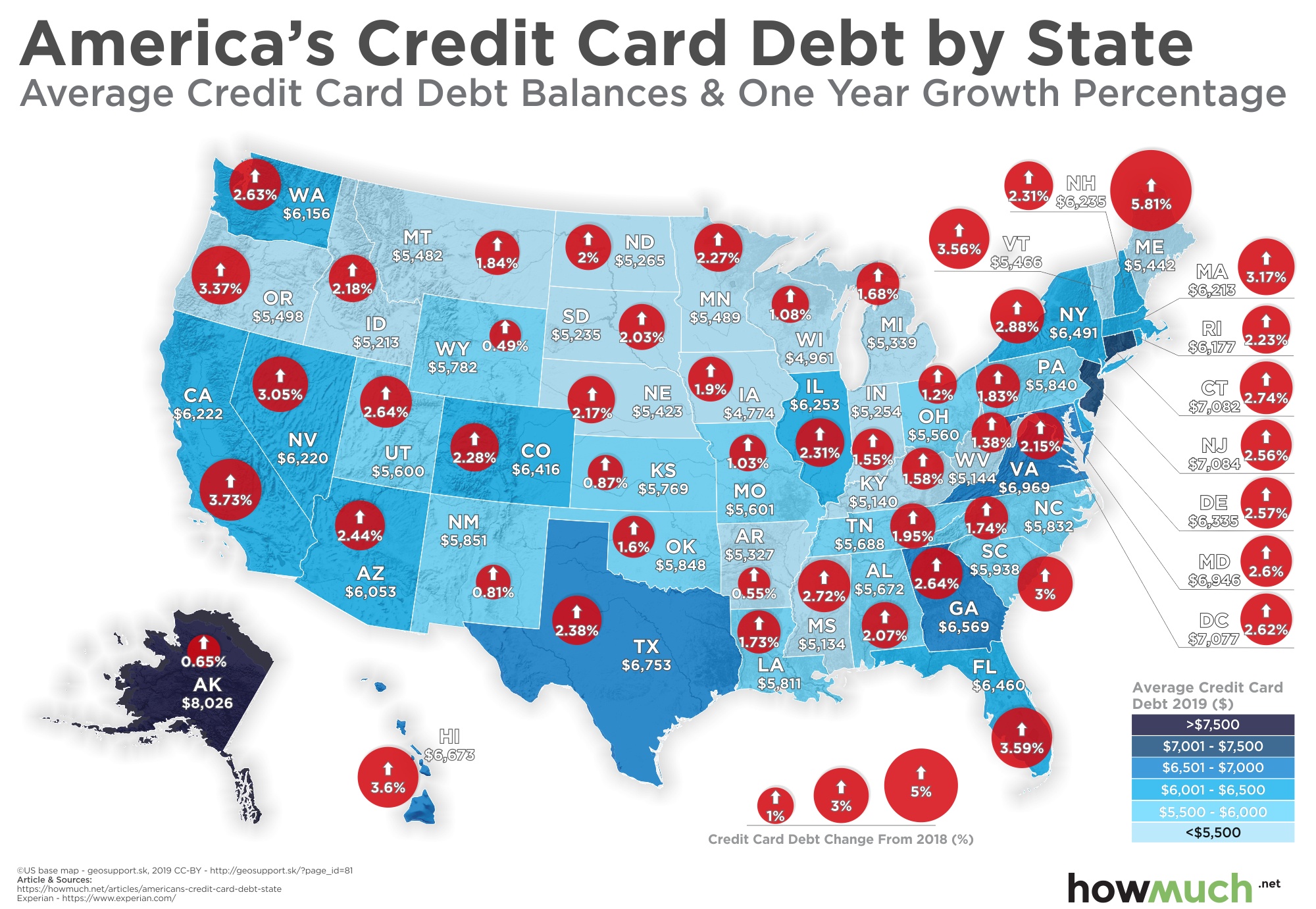

The data comes from Experian and compares the average debt in each state as of the second quarter of 2019 versus one year prior. A darker shade of blue on our map viz indicates a higher average debt, and a larger red bubble indicates a greater change from 2018.

Top 10 States With Highest Average Credit Card Debt

1. Alaska: $8,026 (+0.65%)

2. New Jersey: $7,084 (+2.56%)

3. Connecticut: $7,082 (+2.74%)

4. District Of Columbia: $7,077 (+2.62%)

5. Virginia: $6,969 (+2.15%)

6. Maryland: $6,946 (+2.60%)

7. Texas: $6,753 (+2.38%)

8. Hawaii: $6,673 (+3.60%)

9. Georgia: $6,569 (+2.64%)

10. New York: $6,491 (+2.88%)

Credit card debts are up in every state across the country, with annual increases in average debt ranging from 0.49% in Wyoming to 5.81% in Maine. Total average debt ranges from $4,774 in Iowa, to $8,026 in Alaska. Overall cost of living is a large factor in total credit card debt. The states with the highest credit card burdens, such as Alaska and New Jersey, are some of the most expensive states to live in, and Washington DC is one of the most expensive cities to live in. But even in Iowa, the state with the lowest credit card debt, the average balance is nearly $5,000. Compared to the state’s per capita income of about $50,000, this is still a sizable debt.

So what explains the explosion in credit card debt nationwide? Technological convenience is certainly one factor: according to a recent study by debt resolution company Freedom Debt Relief, groceries are the number one reason why people carry a balance. These consumers may do so out of convenience, or for the many perks that accompany many credit cards.

If not repaid promptly, however, even a grocery card bill can morph into a huge payment: individuals with good credit have an average credit card interest rate of 17%, while those with poor credit face average rates of 25%. Store credit cards tend toward 30%, for all borrowers. On top of that, many banks are cutting their credit card perks, while raising rates still higher.

While your bank card’s perks may be cut, it’s unlikely that your bank’s profits will. JPMorgan Chase and Citigroup reported that credit card sales were up 10 and 5 percent, respectively, in the third quarter. Meanwhile, profits at Visa increased 17 percent in its most recent fiscal year, while Mastercard had an 11 percent profit jump in its most recent quarter.

With these rates, it’s no surprise that over one quarter of Americans have more credit card debt than emergency savings. If you are one of the many Americans struggling with credit card debt, start your journey out to financial freedom with our HowMuch guides to bad credit loans and credit card debt consolidation.

Do you prefer to use credit cards for everyday purchases? How much credit card debt is in your state? Let us know in the comments and share with your friends.

Data: Table 1.1

About the article

Authors

Irena - Editor