Business Insurance Cost for Startups

Insurance is essential for any business to safely operate and have a legitimate chance to succeed. Choosing the right policy will comfort your employees and encourage investment and other business partnerships. There are so many factors to consider and types of coverage offered that it all may seem too daunting. This guide to the cost of business insurance for startups will help you make the best decision.

We Cover in This Guide

- How much does business insurance for startups cost?

- What is business insurance for startups?

- What does business insurance for startups cover and NOT cover?

- Who needs business insurance for startups?

- Types of insurance you may need

- Tips for buying

- FAQ

- Summary

How much does business insurance for startups cost?

The cost of business insurance for startups varies considerably based on your industry, details of your business, and coverage. Policies for small businesses with basic coverage can start at $600 per year. Annual rates can be as high as $5,000 for larger businesses with a full range of policies.

What is Business Insurance for Startups?

While a startup might function and feel different from a more mature company, that does not mean that its insurance coverage should be any less comprehensive. If your business faces losses or claims and is unable to cover the cost to pay or defend them, your startup could fold before it gets off the ground. Business insurance for startups will cover such scenarios, protecting your business and giving you a chance to succeed.

What Does Business Insurance for Startups Cover and NOT Cover?

Business insurance for startups protects a company from claims including:

- On-site accidents

- Loss or theft of office equipment, supples, and inventory

- Lawsuits for defamation of character

- Lost revenue if the business is interrupted during a covered claim

- Professional errors

- Employee injuries or illness

Your specific coverage will depend on the policy package you choose.

Despite the many general policies offered, certain risks, like flood damage, are not covered without that particular insurance.

Additionally, business insurance for startups alone does not cover your personal assets if you operate as a sole proprietor. This enterprise means you will be personally responsible for any losses and claims against the company. You can protect yourself by forming a limited liability company (LLC) to separate the assets and liabilities of your business from your own.

Who Needs Business Insurance for Startups?

Startups are extremely fragile in their infancy, and big losses or damages could shut a business down. If any of the following apply to your startup, you need business insurance:

- Work with customers or clients

- Own business property

- Rent business equipment

- Have assets

- Advertise

- Have employees

- Provide advice or service

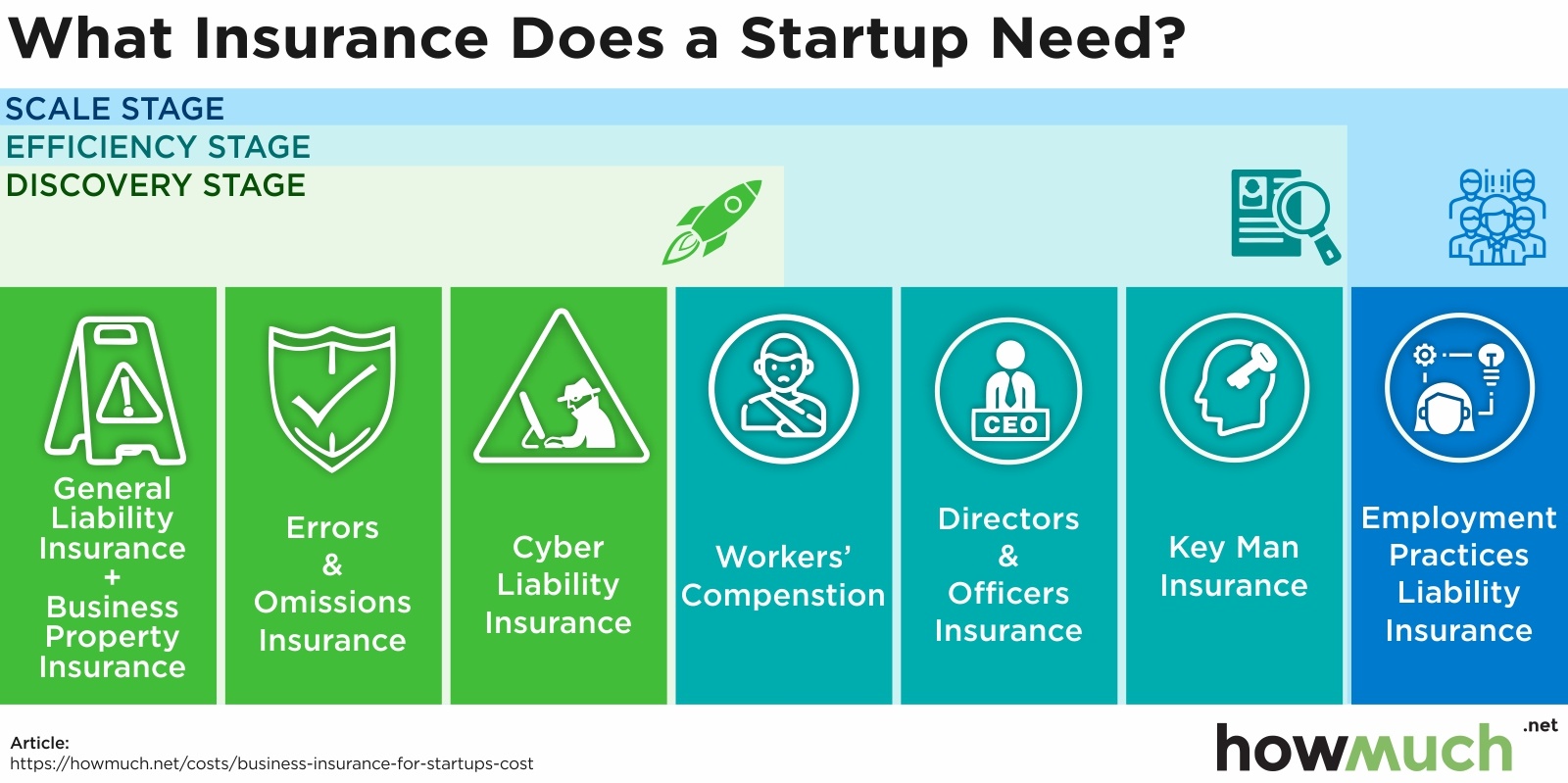

Types of Insurance You May Need

The types of coverage your startup may need is dependent on your industry, risks, and the stage of your company’s development.

The first stage is Discovery. Startups in this category are self-funded or F&F, have no or few employees, and are developing a product. If your company is in this stage, you will need the following policies:

- General Liability Insurance: Protects your company against claims from injury, property damage, or losses from accidents on your property or harm caused by your product or services.

- Property Insurance: Provides coverage for your physical assets in case of loss or damage. The policy will typically pay to replace or repair the item and cover lost income from service interruption.

- Cyber Liability Insurance: Covers your financial losses resulting from data breaches and other cyber incidents. Policies may protect you from damages caused directly by your company (first-party) and harm from an outside source as a result of your company’s negligence (third-party).

The next stage is Efficiency. Your company has achieved this milestone if you have raised more than $1 million, you are actively hiring, and you have launched your product. With these achievements, you need:

- Workers’ Compensation Insurance: This policy covers the treatment and lost wages of an employee who gets ill or injured while on the job. (This may have already been needed in the first stage.)

- Directors and Officers Insurance: Covers your founders, executives, and members of the board of directors against claims of wrongful acts, management misconduct, theft, unfair competition, fraud, and more.

- Key Man Insurance: A life insurance policy that a startup purchases on a key executive’s life. The company is the beneficiary.

The final stage is Scale. This is when you have moved along several rounds of funding, have an HR department, and your revenues and client base are scaling. At this level, you then need:

- Employment Practices Liability Insurance: Covers claims by employees that their legal rights have been violated. Such rights can include sexual harassment, discrimination, and wrongful termination.

Tips for Buying

- Compare quotes: Policy costs can vary between insurance providers. Work with an independent agent to get multiple quotes with one application and compare rates before signing a policy.

- Plan ahead: Anticipating your needs and purchasing certain coverages early may prevent work interruption and could save money on premiums.

- Bundle policies: Insurers will often provide discounted rates when you combine certain key coverages.

FAQ

Why does my startup need business insurance?

Startups are vulnerable; early losses or a lawsuit can quickly take down a new company. Despite the cost of business insurance for startups, the protection it provides more than pays off.

Is business insurance mandatory for startups?

In general, business insurance is optional for startups, but investors, clients, and third parties often require certain coverage. Additionally, most states require workers’ compensation insurance.

Why is insurance for startups important?

Insurance provides peace of mind and helps your company grow by engaging investors, keeping your customers feeling safe, and attracting top talent.

Summary

Business insurance is essential for any startup. The risks and potential liabilities remain the same whether or not your company is profitable, and the stakes of a financial setback are even higher. By understanding the cost of business insurance for startups and determining the needs of your company at each development stage, you can assemble a policy that covers all your potential risks and feel secure knowing that your business is protected and has an opportunity to succeed.