The single biggest expense in most people’s budgets is for housing. Whether renters or homeowners, personal finance experts agree that a housing payment should ideally be no more than 30% of income. If you spend more than that, the government considers housing to be a financial burden. So what does the situation look like across the country? We found the numbers for our maps from the Joint Center for Housing Studies (JCHS) at Harvard University, which publishes an annual analysis of housing trends and figures. We created a series of heat maps corresponding to the metro areas where a significant share of the population (25% or more) face a burden to pay for housing.

We found the numbers for our maps from the Joint Center for Housing Studies (JCHS) at Harvard University, which publishes an annual analysis of housing trends and figures. We created a series of heat maps corresponding to the metro areas where a significant share of the population (25% or more) face a burden to pay for housing.

Top 10 Metro Areas Where Americans Struggle to Afford Their Homes

1. Los Angeles, CA: 46.7%

2. Miami, FL: 45.7%

3. San Diego, CA: 43.2%

4. New York, NY: 43%

5. San Bernardino, CA: 42.9%

6. Fresno, CA: 41.2%

7. Ventura, CA: 40.4%

8. Honolulu, HI: 40.3%

9. Bridgeport, CT: 38.9%

10. Bakersfield, CA: 38.8%

An obvious trend is immediately obvious looking across the entire country: housing burdens are significantly more prevalent on the coasts as compared to the Midwest and the South, and in particular California and the Northeast. Don’t get us wrong—housing burdens are in every region. But in fact, 6 out of the top 10 metro areas with the highest percentage of people burdened by housing costs are in California, topping out at 46.7% in Los Angeles. That means almost every other person is struggling to keep a roof over their head in LA. Clearly these places have incredibly high demand for housing combined with comparatively low incomes for most people.

Taking a closer look at the Southwest reveals the extent of the problem. Stretching from San Francisco along the Pacific toward San Diego, between 30-45%+ of the population struggle to pay for housing. San Jose represents a fascinating case study of inequality. The average household income is $109,200, and yet 36.5% of people have trouble paying for their homes. In a word, that’s due to gentrification. People with high-paying jobs in Silicon Valley can afford to pay expensive prices, but that drives up the prices for everybody else too.

Taking a closer look at the Southwest reveals the extent of the problem. Stretching from San Francisco along the Pacific toward San Diego, between 30-45%+ of the population struggle to pay for housing. San Jose represents a fascinating case study of inequality. The average household income is $109,200, and yet 36.5% of people have trouble paying for their homes. In a word, that’s due to gentrification. People with high-paying jobs in Silicon Valley can afford to pay expensive prices, but that drives up the prices for everybody else too.

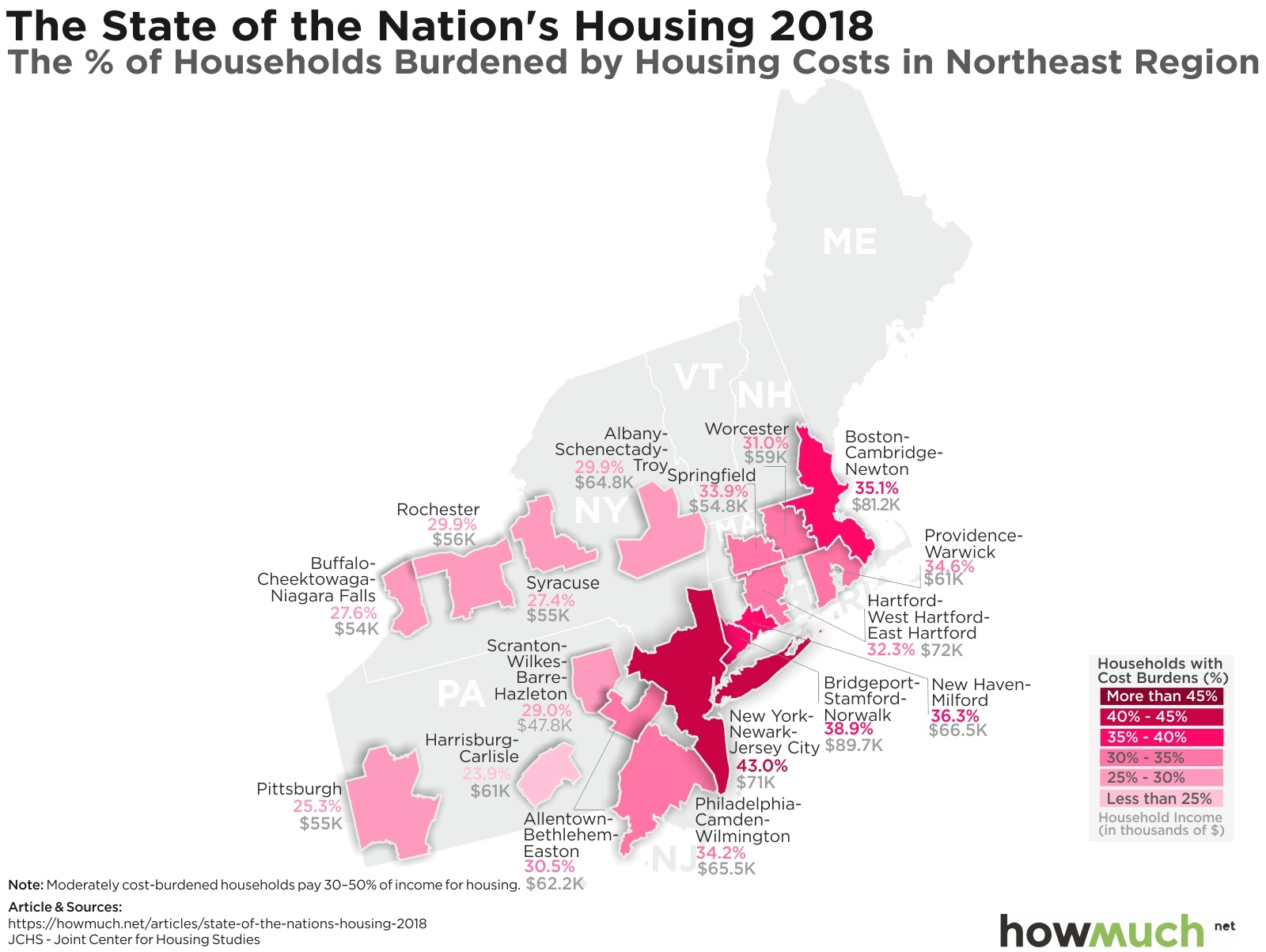

The situation is similar across pockets of the Northeast, in particular in the greater New York and Boston areas. Places like Bridgeport, CT have comparably high average household incomes ($89,700) but shockingly high figures for housing cost burdens (38.9%). Let’s spare a thought for Pittsburgh, though, where the average household makes significantly less at $55,000 and 25.3% of the population struggles to pay for housing. These numbers hint at the pockets of poverty that exist in old manufacturing centers.

The situation is similar across pockets of the Northeast, in particular in the greater New York and Boston areas. Places like Bridgeport, CT have comparably high average household incomes ($89,700) but shockingly high figures for housing cost burdens (38.9%). Let’s spare a thought for Pittsburgh, though, where the average household makes significantly less at $55,000 and 25.3% of the population struggles to pay for housing. These numbers hint at the pockets of poverty that exist in old manufacturing centers.

Speaking of the Rustbelt, take a look across the Midwest. Chicago immediately stands out as the place with the highest share of housing burdens at 35.0%, which is several points above every other metro area in the region. The city with the highest average incomes is further north in Minneapolis-St. Paul at $71,700. The relatively low rates of housing burdens combined with reasonable income levels makes us believe the Midwest is the best overall place for housing in the country.

Speaking of the Rustbelt, take a look across the Midwest. Chicago immediately stands out as the place with the highest share of housing burdens at 35.0%, which is several points above every other metro area in the region. The city with the highest average incomes is further north in Minneapolis-St. Paul at $71,700. The relatively low rates of housing burdens combined with reasonable income levels makes us believe the Midwest is the best overall place for housing in the country.

Taking a look across the South demonstrates a slightly worse situation than the Midwest. There are clearly several metro areas with significant problems, notably Virginia Beach (35.2%), New Orleans (36.2%), Orlando (37.6%) and Miami (45.7%). But what stands out to us is actually McAllen, TX, along the US-Mexico border. 31.8% of the population struggle to pay for housing on average incomes of only $36,700. These numbers indicate a severe level of poverty combined with a shortage in affordable living spaces.

Taking a look across the South demonstrates a slightly worse situation than the Midwest. There are clearly several metro areas with significant problems, notably Virginia Beach (35.2%), New Orleans (36.2%), Orlando (37.6%) and Miami (45.7%). But what stands out to us is actually McAllen, TX, along the US-Mexico border. 31.8% of the population struggle to pay for housing on average incomes of only $36,700. These numbers indicate a severe level of poverty combined with a shortage in affordable living spaces.

There are two sides to the equation when it comes to affordable housing: income levels and housing costs. Expensive housing may in itself not be a burden if everyone has enough money to support the market. And making relatively little money doesn’t necessarily mean someone is burdened by housing costs if it takes only a couple hundred dollars to pay the rent. Unfortunately, there’s been significant pressure on both sides of the equation. As the JCHS notes, “The national median rent rose 20 percent faster than overall inflation between 1990 and 2016 and the median home price rose 41 percent faster.” And over the last 20 years, inflation-adjusted median household incomes have only barely grown to about $59,000. The combination of rising housing costs and stagnant wage growth indicates that the crisis in affordable housing will endure for many more years.

Data: Table 1.1

About the article

Authors

Irena - Editor